Why Singapore private bank onboarding is suddenly in focus

Singapore has become one of Asia's most important wealth management hubs. More high-net-worth families, entrepreneurs, external asset managers, and single family offices are using Singapore as a base for investment holding, succession planning, banking access, and regional business activity.

The frustration is that private bank onboarding can still feel painfully slow. A client may have a legitimate business exit, a reputable adviser, and a clean transfer from another bank, yet still spend weeks answering source-of-wealth questions and supplying supporting documents.

On 25 May 2026, Channel NewsAsia reported that Singapore private banks and regulators are working on faster account-opening processes for wealthy clients, including standardised forms and a target of reducing some account-opening timelines from several months to under one month by the end of 2026. [15 Jun 2026 update] Two weeks later, on 12 June 2026, MAS confirmed a second, related move: its revised framework for Single Family Offices takes effect on 15 June 2026. Both point the same way - less administrative friction. Neither removes the hardest question: can the bank understand how the wealth was actually created?

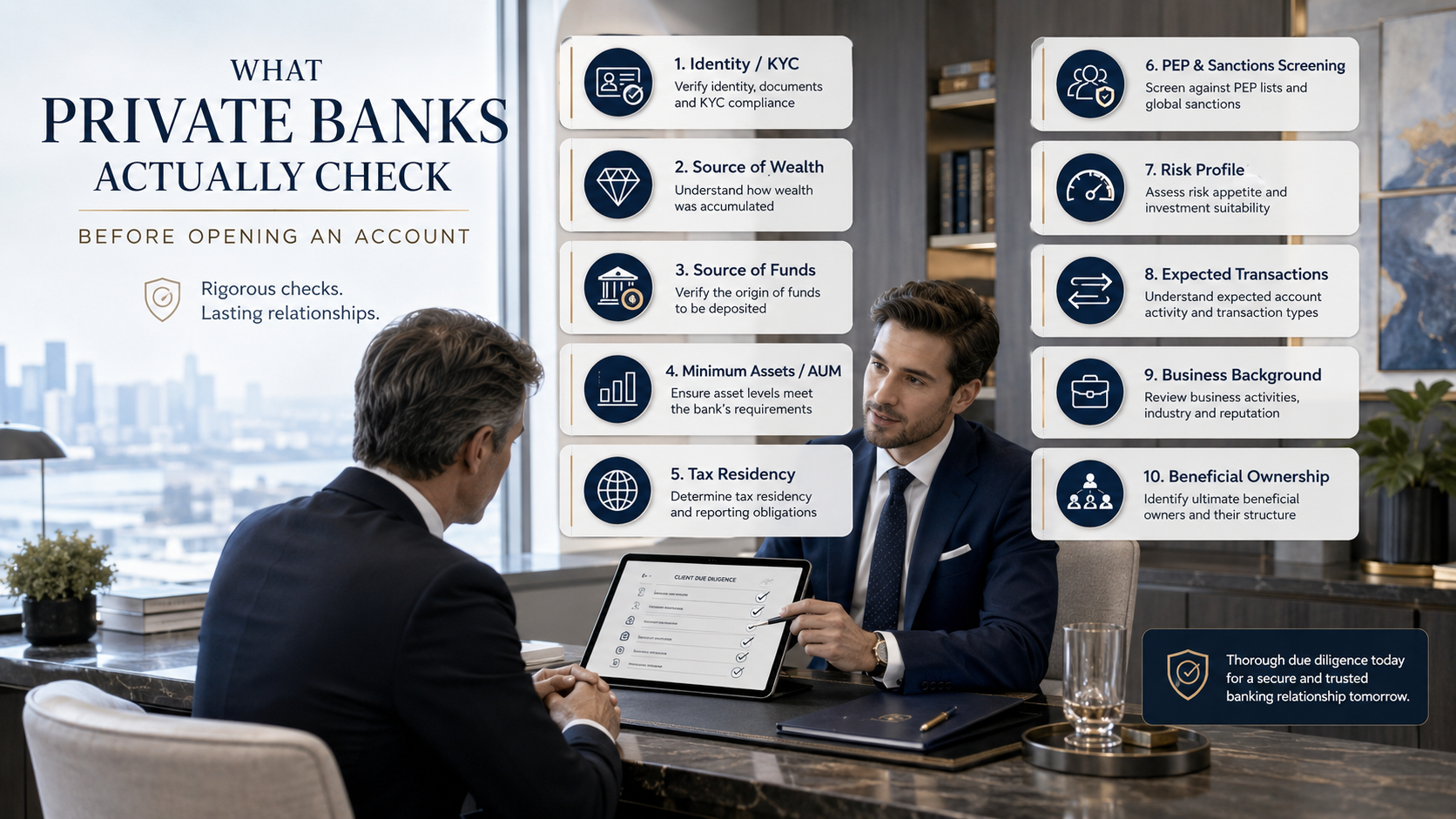

What private banks actually check before opening an account

A private bank is not just opening a savings account. It is taking a view on the client's identity, beneficial ownership, source of funds, source of wealth, tax position, sanctions exposure, politically exposed person exposure, expected account activity, and reputational risk.

Source of funds explains where a specific deposit came from. Source of wealth explains how the client built their overall net worth over time. A clean bank transfer can satisfy one question and still leave the other unanswered.

| Wealth origin | Documents commonly requested | What the bank is testing |

|---|---|---|

| Business ownership | Audited accounts, company registry profiles, shareholder records, dividend history | Whether the business can plausibly support the stated wealth |

| Company sale or liquidity event | Sale and purchase agreement, board resolutions, receipt bank statements, tax filings | Whether proceeds match the transaction story |

| Executive compensation | Employment contracts, payslips, tax returns, bonus letters, equity award records | Whether income history explains accumulated wealth |

| Investment gains | Brokerage statements, custodian statements, transaction history, capital injection records | Whether the portfolio was accumulated legitimately over time |

| Inheritance or family wealth | Will, probate documents, trust deeds, family business documents, benefactor wealth evidence | Whether the original source of family wealth can be understood |

| Property gains | Title deeds, option agreements, completion statements, valuation reports, rental records | Whether gains and sale proceeds reconcile with market and bank records |

The red flags that slow everything down

Most delays are not caused by one missing document. They come from a story that does not reconcile cleanly across documents, jurisdictions, entities, and time.

Opaque entities

Offshore companies and trusts can be legitimate, but the client must explain the commercial, tax, or succession reason for the structure.

Third-party funding

Transfers from unrelated parties, money service businesses, or intermediaries with no clear nexus often trigger enhanced due diligence.

Weak wealth narrative

A declared net worth must make sense against age, career path, business record, geography, and available documents.

Compliance teams should still apply judgement. Legitimate entrepreneurs from emerging sectors or markets may have wealth stories that look unusual on paper. Unusual is not the same as suspicious, but it does need clearer explanation.

How Singapore is trying to make onboarding faster

The most practical reform is standardisation. When each bank asks for different documents in different formats, clients and external asset managers waste time producing the same evidence repeatedly. Common forms and clearer documentation expectations should reduce unnecessary back-and-forth. The revised Single Family Office framework adds a second track: a simpler, more predictable route to the licensing exemption that most SFOs rely on.

| Reform area | What it improves | What it does not solve |

|---|---|---|

| Standardised onboarding forms | Reduces duplicate and inconsistent requests across banks | Does not remove the need for proper source-of-wealth evidence |

| RegTech and screening tools | Speeds up beneficial ownership mapping, sanctions checks, PEP checks, and adverse media review | Can still produce false positives and requires human review |

| Digital identity and data infrastructure | Helps Singapore-linked clients verify identity and entity data faster | May be less helpful for foreign clients with overseas documents and complex structures |

| 15 Jun 2026 update Revised SFO licensing framework effective 15 Jun 2026 | Replaces case-by-case licensing exemption with a structure-agnostic class exemption; qualifying SFOs notify MAS, hold a MAS-licensed bank account, and file an annual return | Does not relax bank onboarding or source-of-wealth checks because the mandatory bank account keeps AML scrutiny at the bank level |

In other words, Singapore is trying to remove administrative friction, not lower the bar. For clean cases, this should help. For complex cases, the old questions remain: who owns the assets, how did the wealth arise, and does the story hold together?

MAS confirmed on 12 June 2026 that its revised framework for Single Family Offices takes effect on 15 June 2026. For the families this article is written for, the practical shift is that the regulatory side of standing up an SFO is now lighter and more predictable - while bank onboarding remains central because holding a MAS-licensed bank account is now a condition of the exemption itself.

What the revised Single Family Office framework actually requires

From 15 June 2026, a qualifying SFO no longer applies for a case-by-case licensing exemption. It falls under a single, structure-agnostic class exemption from the fund-management licensing requirement under the Securities and Futures Act. In return, the SFO takes on a short set of standing obligations.

- Notify MAS within 14 days of commencing business in Singapore.

- Obtain a legal opinion from a Singapore law firm confirming the SFO meets the qualifying criteria for the class exemption.

- Maintain an account with a MAS-licensed bank.

- File an annual return within four months of the SFO's financial year-end, stating total assets under management and the MAS-regulated financial institutions it banks with.

Existing SFOs have a one-year transitional period, until 15 June 2027, to move onto the revised framework. Note the two separate timing points people tend to confuse: 14 days applies to the initial notification, while the annual return is due within four months of the financial year-end.

SFO licensing exemption

This framework lets the office manage family money without a capital markets services licence, if the class exemption conditions are met.

13O and 13U tax incentives

These remain separate applications with their own AUM, local spending, investment-professional, and MAS approval requirements.

Private bank onboarding

The bank's KYC, AML, and source-of-wealth review remains a separate gate. Clearing one door does not clear the other two.

The headline reform removes paperwork at the regulator, but the framework makes a MAS-licensed bank account a standing condition of the exemption. The licensing bottleneck moves; it does not disappear. For complex, multi-jurisdiction families, the binding constraint was rarely the MAS form. It was the banker's question: can the wealth story be understood, documented, and defended?

MortgageLogic Advisory

Speak with us before you structure the next move

MortgageLogic Advisory is not a private bank and does not open private bank accounts. What we do is help families, business owners, and property investors think through financing readiness, property-backed liquidity, family office planning, and the documents that often sit around a banking or wealth-structuring conversation.

- Review property and business financing options before major wealth moves

- Map lending capacity before family office or investment restructuring

- Prepare a practical document checklist for mortgage, SME, or property-backed loan discussions

- Coordinate next steps around bank lending, property financing, and wealth planning

Speed vs integrity: the uncomfortable trade-off

Faster onboarding is not the same as easier onboarding. That distinction matters. Singapore's reputation as a wealth hub depends on being efficient enough for legitimate clients and strict enough to deter questionable money.

The 2023 Singapore money laundering case, which later led to penalties against financial institutions for AML/CFT control lapses, is the reminder. The weakness in bad cases is rarely a missing PDF. It is a convincing-looking paper trail that hides the wrong risk. [15 Jun 2026 update] It is also why the revised SFO framework keeps a MAS-licensed bank in the loop for every family office. The monitoring did not loosen; it was re-routed through the banks.

Who benefits most from the faster onboarding push?

Clean family office structures

Families with transparent entities, clear tax residency, and documented wealth should see the biggest improvement, and the clearest path through the new class exemption.

External asset managers

EAMs coordinating several bank relationships benefit when document requests become more predictable.

Singapore as a wealth hub

Shorter timelines help Singapore compete with Hong Kong, Switzerland, Dubai, and Luxembourg for legitimate capital.

Clients with complex multigenerational structures, high-scrutiny jurisdictions, old wealth with poor historical records, or unconventional crypto and startup gains may still face deeper questioning. The process may become faster, but difficult cases will not become simple overnight.

MortgageLogic view: speed is a feature, integrity is the product

Singapore is right to remove repetitive paperwork and inconsistent documentation requests. Genuine families should not need to answer the same question three different ways because each bank uses a different form, and a qualifying SFO should not need a bespoke licensing exemption when a clear class exemption will do.

But the real product Singapore is selling is trust. Faster onboarding and a lighter licensing route only work if the source-of-wealth review remains credible. The best outcome is a system that lets clean wealth move faster and identifies bad actors more intelligently.

For clients, the practical lesson is simple: prepare the narrative before the bank asks. If the source-of-wealth story is coherent, documented, and consistent with the structure, the account-opening conversation becomes easier. If the story is vague, speed will only deliver a faster rejection.

FAQ

FAQ About Singapore Private Bank Onboarding

What changed for single family offices on 15 June 2026?

MAS replaced the old case-by-case licensing exemption with a single, structure-agnostic class exemption from fund-management licensing. A qualifying SFO now notifies MAS within 14 days of commencing business, obtains a legal opinion from a Singapore law firm that it meets the criteria, maintains an account with a MAS-licensed bank, and files an annual return within four months of its financial year-end reporting total AUM and its banking relationships. Existing SFOs have until 15 June 2027 to transition.

Does the new class exemption make private bank onboarding faster?

Not directly. The class exemption simplifies the licensing step at MAS. It does not relax a bank's own KYC, AML and source-of-wealth checks. Because the framework requires every qualifying SFO to maintain a MAS-licensed bank account, that onboarding review remains a hard requirement. A well-prepared source-of-wealth narrative still does more to speed up account opening than the exemption does.

Why does private bank onboarding in Singapore take so long?

Private banks must verify identity, beneficial ownership, sanctions and PEP exposure, source of funds, source of wealth, tax residency, account purpose, and expected transaction profile. Multi-jurisdiction family office structures add complexity because the bank must understand the entities behind the account, not just the person signing the forms.

What is the difference between source of funds and source of wealth?

Source of funds explains where a specific deposit came from. Source of wealth explains how the client built their overall net worth over time. A transfer from another reputable bank may support source of funds, but it may not prove how the money was originally earned.

Will faster onboarding mean lower AML standards?

The stated direction is faster processing without lowering AML and KYC standards. Standard forms, better technology, and clearer document expectations can shorten administrative delays, but higher-risk clients should still expect enhanced due diligence.

Who benefits most from streamlined private banking onboarding?

The clearest beneficiaries are clients with clean, well-documented wealth from Singapore or other lower-risk jurisdictions, established family offices with transparent structures, EAMs coordinating several bank relationships, and relationship managers trying to reduce repeated paperwork.

Important disclaimer

This article is for general information only and does not constitute financial, legal, tax, compliance, investment, or private banking advice. MortgageLogic Advisory does not open private bank accounts and does not represent any private bank. Readers should consult their bank, legal adviser, tax adviser, compliance adviser, or licensed wealth professional for personalised guidance. Regulatory details, including the operation of the revised SFO framework, should be verified against official MAS guidance before being relied upon.

Sources checked

- MAS: Revised Framework for Single Family Offices to take effect on 15 June 2026

- MAS: Response to Feedback on Proposed Framework for Single Family Offices

- EDB: Guide to Setting Up a Single Family Office in Singapore

- CNA: Singapore private banks to speed up account opening for wealthy clients

- ACIP / ABS: Best Practice Paper on Source of Wealth Due Diligence

- CNA: MAS penalties linked to Singapore's 2023 money laundering case